Nigeria maintained its position as the world’s third-largest borrower from the International Development Association (IDA), the concessional lending arm of the World Bank, in the first quarter of 2026. While the headline figure showed a slight decline in debt exposure, the broader picture told a more complex story, one of a nation balancing ambitious development goals against an increasingly heavy debt burden.

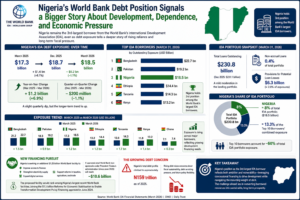

Fresh financial statements released by the IDA for March 2026 showed Nigeria’s exposure stood at $18.5 billion as of March 31, a marginal decline from the $18.7 billion recorded at the end of December 2025. The reduction of approximately $200 million represented a modest 1.1 percent drop over three months, suggesting a temporary pause rather than a fundamental shift in borrowing patterns.

Beneath that quarter-on-quarter decline, however, sat a more revealing trend. Compared with the same period a year earlier, Nigeria’s exposure rose significantly from $17.3 billion in March 2025, marking a $1.2 billion increase and reinforcing a trajectory that has steadily moved upward. The figures reflected a country increasingly leaning on concessional financing as it attempts to fund reforms, infrastructure projects, social investment programs, and broader economic restructuring.

YOU CAN ALSO READ: How TUBO Became the Creative Force Behind Olori Ivie Emiko’s Royal Identity

The latest IDA rankings placed Nigeria behind Bangladesh and Pakistan among the World Bank’s largest borrowers. Bangladesh retained its position at the top with $22.7 billion in exposure, while Pakistan followed with $19.2 billion. Nigeria occupied third place with $18.5 billion, ahead of several major African economies.

Across the continent, Ethiopia held exposure of $14.4 billion, Tanzania followed closely with $14.3 billion, while Kenya stood at $13.2 billion. The numbers highlighted the extent to which many developing economies increasingly rely on multilateral institutions to finance growth and address structural challenges.

Globally, the IDA’s loan portfolio showed only slight movement. Total outstanding loans stood at $230.8 billion as of March 2026, down marginally from $231.1 billion three months earlier. The institution described the decline as a mild moderation in its lending activity rather than a significant contraction.

Importantly, the quality of the loan book remained relatively strong. Non-accrual loans, those where repayment difficulties exist, represented only 0.4 percent of the total portfolio. Provisions for potential loan losses stood at $6.3 billion, accounting for around 2 percent of underlying exposures.

Nigeria alone accounted for nearly 8 percent of the IDA’s total portfolio and approximately 13.3 percent of the combined exposure represented by the institution’s ten largest borrowers. Collectively, those top ten countries made up nearly 60 percent of the IDA’s overall lending exposure, underscoring how a relatively small group of economies now absorbs a substantial portion of concessional financing globally.

For Nigeria, the numbers reflected more than debt statistics; they revealed the scale of the country’s financing demands.

Africa’s largest economy continues to face enormous infrastructure deficits, energy constraints, social spending pressures, and reform financing needs. Population growth, urban expansion, and persistent development gaps have all increased pressure on public resources. In that environment, concessional financing often appears to policymakers as one of the few available avenues for sustaining investment without turning immediately to more expensive commercial debt markets.

Reports indicated that the Federal Government is pursuing an additional $1.25 billion World Bank facility designed to improve access to finance, strengthen electricity supply, expand digital services, and support reforms spanning taxation, agriculture, and trade. If approved, the facility would raise total World Bank loan approvals secured under President Bola Ahmed Tinubu’s administration since June 2023 to approximately $10.6 billion.

The proposed financing would rank among Nigeria’s largest recent World Bank facilities, joining major approvals such as the $1.5 billion Reforms for Economic Stabilisation to Enable Transformation Development Policy Financing package approved in June 2024.

Supporters argue that such financing remains necessary to fund reforms capable of unlocking long-term economic productivity. Critics, however, increasingly warn that Nigeria may be approaching a dangerous threshold.

The concern is not merely the volume of borrowing but its cumulative effect on future fiscal flexibility.

As Nigeria’s overall debt profile climbed to approximately N159 trillion in 2025, economists and financial analysts raised fresh concerns about sustainability. Questions increasingly centered on whether rising obligations could eventually constrain public spending, increase debt servicing pressures, and limit future policy options.

YOU CAN ALSO READ: “Whoever Feeds You Can Enslave You”: Obasanjo’s Stark Warning on Africa’s Future

Among those raising concerns was finance expert and senior partner at SPM Professionals, Dr. Paul Alaje, who argued that the burden of today’s borrowing would extend well beyond current generations.

He noted that the country’s expanding debt obligations would ultimately be borne by Nigerians for years to come, including future citizens yet unborn. He warned that while debates often focus on borrowing capacity, a more pressing question may involve the long-term economic cost of accumulating liabilities at such pace.

His observations reflected a broader debate unfolding across Nigeria: whether multilateral financing represents a strategic instrument for development or whether dependence on external borrowing risks creating deeper vulnerabilities.

For now, Nigeria’s standing as the World Bank’s third-largest IDA borrower illustrates both realities at once, a nation pursuing transformation through development financing while simultaneously navigating the mounting weight of debt that accompanies it.